See the tax-free retirement income most plans miss

WealthPath now models the Guaranteed Income Supplement year by year — and warns you before a routine RRIF withdrawal quietly erases it.

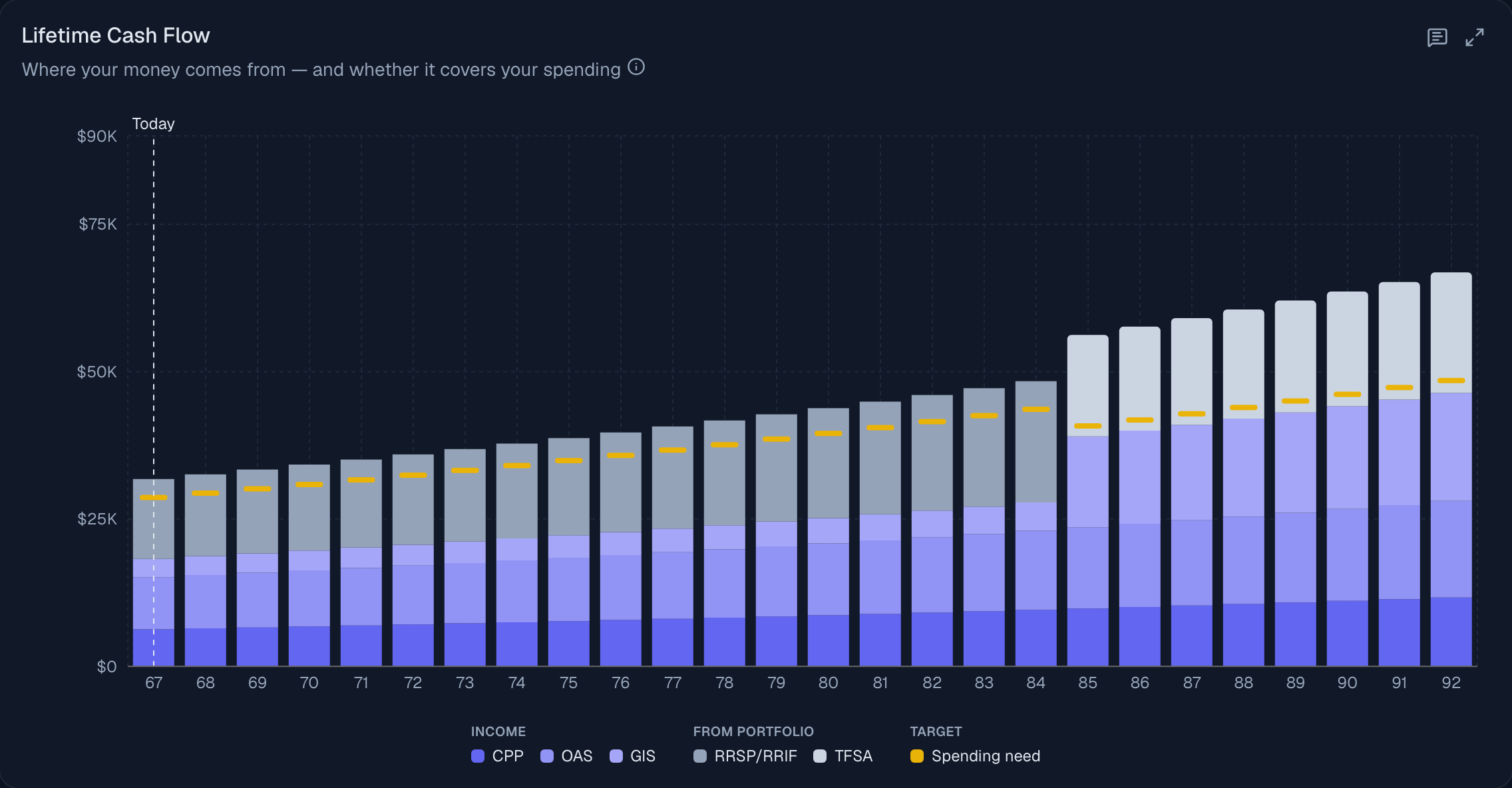

Lifetime cash flow — GIS stacked with CPP and OAS across every year of retirement.

For lower-income Canadian retirees, the Guaranteed Income Supplement can be worth more than $13,000 a year, entirely tax-free. But it's income-tested: every dollar drawn from an RRSP or RRIF can claw it back — and the mandatory RRIF minimum that kicks in at 72 can erase thousands of it in a single year.

Most planning tools don't model GIS at all. So the most consequential trade-off a low-income retiree faces stays invisible — until it's too late to plan around.

GIS now lives inside your projection

WealthPath estimates your entitlement for every year of retirement — single or couple — using the published income-tested schedule, recalculated as your income changes and indexed to inflation. It sits right in your income waterfall, so the benefit and the withdrawals that erode it finally live in one place.

Income-tested, recalculated every year

Each year's GIS is estimated from your projected income using the published reduction schedule — about $1 less for every $2 of non-OAS income. WealthPath applies the single rate, or the combined-income couple rate when both partners receive OAS, then indexes the maximum to inflation. Non-taxable, and updated automatically as your plan changes.

The full calculation trail — GIS estimated for each year, beside CPP and OAS.

See the RRSP/RRIF trade-off

GIS appears as its own band in your cash-flow chart and a column in the full calculation trail, stacked alongside CPP and OAS. The moment a withdrawal pushes your income up, you can watch the benefit shrink — no spreadsheets, no guesswork, just the real cost of a drawdown decision.

Get warned before it's gone

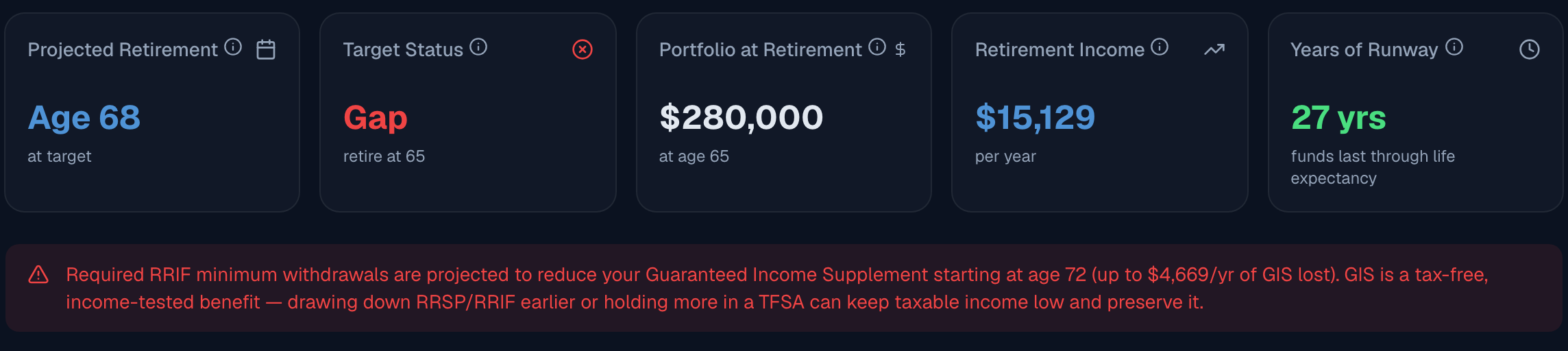

When projected RRIF minimums are set to reduce or eliminate your GIS, WealthPath flags it — with the age it starts, the dollars at stake, and the lever to fix it: draw down earlier, or hold more in a TFSA to keep taxable income low.

An automatic alert when mandatory RRIF minimums will erode your GIS.

Changelog · GIS (FEAT-002 §1)

- New entitlement model — single ($13,042.56/yr) and couple-both-OAS ($7,850.76/yr) maxima, 2025-anchored, inflation-indexed.

- Computed per year in both single and household projections; testable income = net income excluding OAS.

- Surfaced in the All-Data table, lifetime totals, and the cash-flow income chart; treated as non-taxable throughout.

- Automatic RRIF→GIS erosion warning with the onset age and annual amount at risk.

- 16 new unit + integration tests; full suite green (lint, types, build, e2e).